El fabricante estadounidense de coches eléctricos Tesla registró un beneficio neto atribuido de 1.129 millones de dólares en el primer trimestre del año, lo que supone una reducción del 55% en comparación con los 2.513 millones de dólares contabilizados en el mismo periodo de 2023, según las cuentas presentadas por la compañía.

En ese sentido, el margen operativo de la compañía cerró el primer trimestre del año en el 5,5%, lo cual supone 5,9 puntos porcentuales menos que en el mismo periodo del año anterior, cuando se situó en el 11,4%.

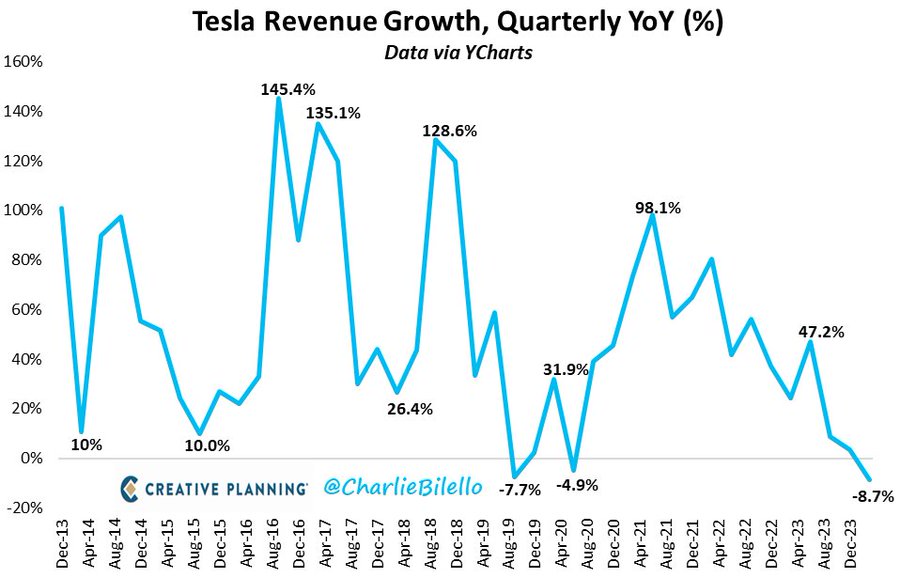

Asimismo, la compañía que lidera Elon Musk ha disminuido sus ingresos hasta los 21.301 millones de dólares en el primer trimestre del año, un 9% menos que los 23.329 millones de dólares que facturó entre enero y marzo de 2023.

Asimismo, el resultado bruto de explotación (Ebitda) ajustado hasta marzo fue de 3.384 millones de dólares, un 21% menos que los 4,267 millones de dólares del primer trimestre de 2023.

Tesla justifica esta disminución de los volúmenes a la actualización de su rampa de producción del Modelo 3 en la fábrica de Fremont (California) y a los "cierres de fábrica resultantes de los desvíos de envíos causados por el conflicto del Mar Rojo y un ataque en la Gigafactory de Berlín", explica el comunicado.

Además, la compañía del magnate ha adelantado que actualizará su futura gama de vehículos en los que se incluirán modelos más asequibles